In the tapestry of life, health emerges as a recurring motif, a thread woven through our experiences, shaping our narratives and influencing our trajectories. As we navigate the complexities of aging, the need for reliable healthcare becomes increasingly paramount. Within this context, Medicare, a cornerstone of the American healthcare system, provides a safety net, offering crucial coverage for those 65 and older and certain younger individuals with disabilities. Understanding the nuances of Medicare, specifically Part A and Part B coverage, becomes a vital step in ensuring access to necessary medical services and safeguarding one's well-being.

Medicare, established in 1965, represents a landmark achievement in social progress. It acknowledges the inherent dignity of individuals and the collective responsibility to ensure access to quality healthcare, regardless of age or economic circumstance. Within the broader Medicare framework, Part A and Part B coverage address distinct yet interconnected aspects of healthcare needs. Part A, often referred to as hospital insurance, covers inpatient hospital stays, skilled nursing facility care, hospice care, and some home health care. Part B, medical insurance, covers services like doctor visits, outpatient care, preventive services, and some medical equipment.

Deciphering the complexities of Medicare Part A and Part B coverage can feel like navigating a labyrinth. Understanding the specifics of what each part covers is crucial for making informed decisions about one's healthcare. For instance, while Part A covers inpatient hospital stays, it doesn't cover all associated costs. Deductibles, coinsurance, and other out-of-pocket expenses may apply. Similarly, Part B typically covers 80% of the Medicare-approved amount for covered services, leaving the beneficiary responsible for the remaining 20% coinsurance.

The origin and evolution of Medicare reflect a societal commitment to the well-being of its citizens. The program's implementation marked a turning point in American healthcare, ensuring that older adults and individuals with disabilities had access to essential medical services. Over time, Medicare has adapted to the changing landscape of healthcare, incorporating new benefits and addressing emerging needs. The introduction of Part D prescription drug coverage in 2006, for example, significantly expanded the scope of Medicare benefits.

One of the central issues related to Medicare Part A and Part B coverage is the issue of affordability. While Medicare provides valuable coverage, it doesn't cover all healthcare costs. Many beneficiaries opt for supplemental insurance, such as Medigap policies, to help cover out-of-pocket expenses. Others may choose Medicare Advantage plans, which are offered by private companies approved by Medicare and provide Part A and Part B benefits, often along with prescription drug coverage.

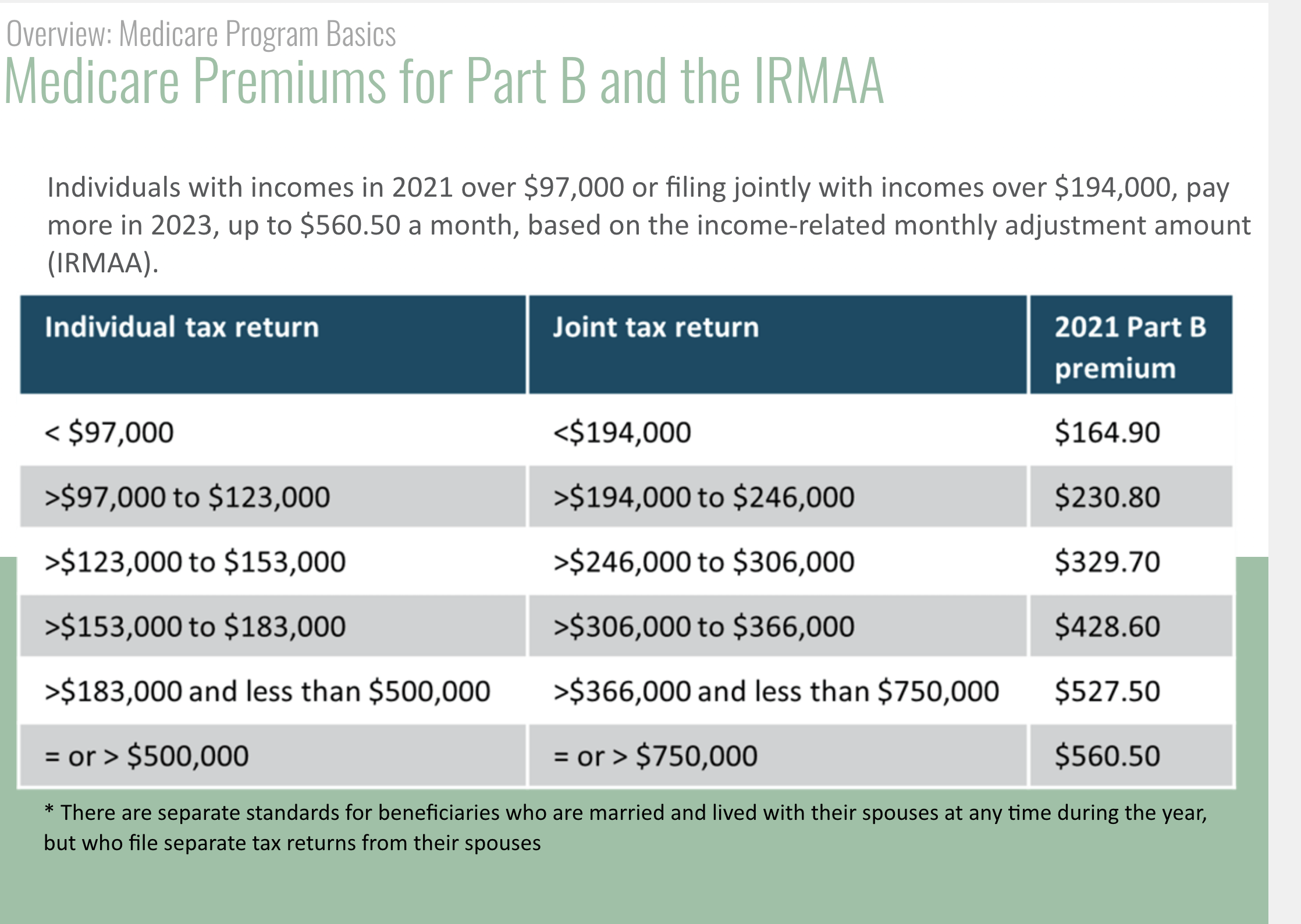

Medicare Part A eligibility is generally automatic for those who qualify for Social Security retirement benefits or Railroad Retirement benefits. Most people don't pay a premium for Part A because they or a spouse paid Medicare taxes while working. Part B, however, does require a monthly premium, which is deducted from Social Security benefits for most beneficiaries.

One benefit of Medicare Part A is access to inpatient hospital care. For example, if a beneficiary requires hospitalization due to a sudden illness or injury, Part A would cover a portion of the hospital stay costs. Part B provides coverage for outpatient services like doctor visits, enabling beneficiaries to receive routine medical care and preventive services. Another benefit is coverage for certain home health services, allowing individuals to receive necessary medical care in the comfort of their own homes.

Advantages and Disadvantages of Original Medicare (Part A & B)

| Advantages | Disadvantages |

|---|---|

| See any doctor who accepts Medicare | No out-of-pocket maximum (can use Medigap) |

| Nationwide coverage | Premiums, deductibles, and coinsurance costs |

| No networks to navigate | Doesn't usually cover prescription drugs (need Part D) |

Frequently Asked Questions:

1. What is the difference between Medicare Part A and Part B?

Part A covers hospital services, while Part B covers medical services.

2. How do I enroll in Medicare Part A and Part B?

You can enroll online, by phone, or in person at a Social Security office.

3. What are the costs associated with Medicare Part A and Part B?

Part A often has no premium, but Part B has a monthly premium, deductibles, and coinsurance.

4. What is Medicare Part D?

Part D covers prescription drugs.

5. What are Medicare Supplement Insurance (Medigap) plans?

Medigap plans help pay some of the out-of-pocket costs not covered by Original Medicare.

6. What are Medicare Advantage plans?

Medicare Advantage plans are offered by private insurance companies and provide Part A and Part B benefits, and often Part D.

7. When can I enroll in Medicare?

You can generally enroll during the Initial Enrollment Period three months before your 65th birthday.

8. Where can I find more information about Medicare coverage?

You can visit the official Medicare website (Medicare.gov) for detailed information.

In the symphony of life, health plays a crucial role, shaping our experiences and influencing our journeys. Medicare, a vital component of the American healthcare system, provides a safety net for millions of individuals, ensuring access to essential medical services. Understanding the nuances of Medicare Part A and Part B coverage is essential for navigating the complexities of healthcare and making informed decisions about one's well-being. By actively engaging with the information available and seeking guidance when needed, individuals can harness the power of Medicare to safeguard their health and navigate the journey of aging with greater confidence and peace of mind.

Unlocking ocean county nj property navigating deeds and titles

Depeche mode electrifies san antonio

Unleash your inner archer the allure of the wood elf ranger in dd